Any content you receive is for information purposes only. Always conduct your own research.

*Sponsored

Game Your Game, Inc. (Nasdaq: GYGY) Just Hit The Top Of Our Screen This Morning — Tuesday, August 11, 2026

Don’t Miss Our Next Update—Get Real-Time Alerts Sent Directly To Your Phone. Up To 10X Faster Than Email. Take A Look At GYGY While It’s Still Early…

August 11, 2026 Dear Reader, If you caught last night's report, you already know why Game Your Game, Inc. (Nasdaq: GYGY) is at the top of our screen this morning — and with less than 90 minutes to the bell, now is the time to take a look. We are talking about a newly listed Nasdaq company with an AI-powered platform sitting inside one of the fastest-growing participation sports in the world. Less than two weeks on the exchange. With under 500K shares listed as available to the public, according to Yahoo Finance data. And a commercial launch that is just getting underway. That is the setup heading into this morning — Tuesday, August 11, 2026 — and GYGY has our full focus right now. When a company has a float that small, the potential exists for big moves if demand begins to shift. What sits underneath this profile? An AI-powered golf technology platform built on over a decade of proprietary shot-level data — and this morning, as GYGY heads into its first full week of active sessions on the Nasdaq, the commercial launch is one session closer to being proven out.

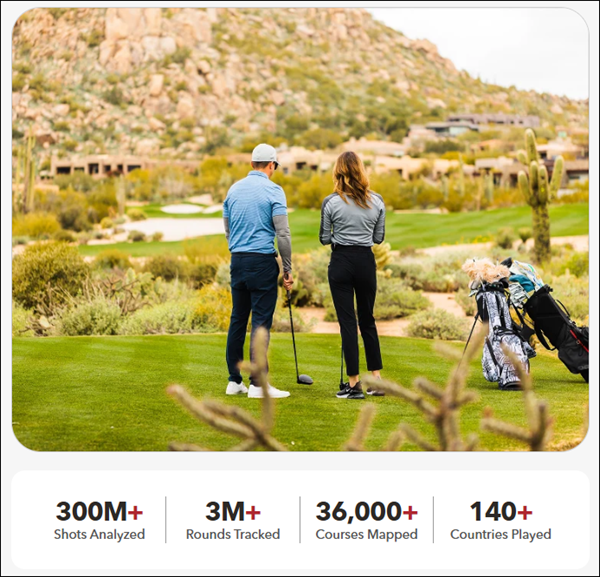

This name completed its Nasdaq direct listing less than two weeks ago, on July 30, 2026. Here is the number that put GYGY at the top of our list tonight: there are less than 500K shares listed as available to the public right now. When a company has a float that small, the potential exists for big moves if demand begins to shift. What sits underneath this profile? An AI-powered golf technology platform with over a decade of proprietary shot-level data — and a commercial launch that is just getting underway. Inside Game Your Game, Inc. (Nasdaq: GYGY) GYGY is headquartered in Palo Alto, California — the heart of Silicon Valley, the world's preeminent technology hub and home to more than thirty Fortune 1000 companies, thousands of promising startups, and one-third of all venture capital in the United States, according to the Center for Strategic and International Studies. The company has been operating in the golf industry since 2014, and in that time its technology has touched golfers in more than 140 countries, mapped over 36,000 golf courses, tracked more than 3M rounds, and captured an estimated 300M+ shots across the lifetime of its platforms.

The product is the GameGolf KZN AI™ platform. Smart sensors mounted on each club use embedded neural network technology to automatically detect and classify every shot, transmitting via Bluetooth to a GPS tracker that pins the shot to its exact location—no manual input, no phone on the course needed. The companion app delivers real-time distances and live scorecards, while the Performance Dashboard surfaces strokes-gained analytics and shot dispersion maps. The AI engine at the center of it all is Smart Caddie—a recommendation layer that pulls from a player’s personal shot history and course context to suggest clubs, target lines, and expected scores in real time.

Revenue comes from two places: hardware sales and recurring subscriptions. Revenue is early-stage and growing fast — the company posted approximately 293% year-over-year growth in its most recent trailing twelve-month period, driven by higher sales of GameGolf KZN devices during beta testing. Management has described the current phase as the transition from beta testing into full commercial launch. And this is where the setup starts to get especially interesting. GYGY is entering its commercial launch with years of platform data already behind it—and a global golf audience numbering well into the 100M+ range directly in front of it. 108M Golfers. One AI Platform. Commercial Launch Now Underway. Golf participation is at its highest level in decades. 48.1M Americans played the sport in 2025, and the R&A estimates more than 108M junior and adult golfers worldwide. That is a global, high-income, equipment-driven customer base that has always spent aggressively on anything that can lower their scores. The technology layer of the sport has shifted dramatically. Shot trackers and connected wearables that once lived exclusively on tour now show up in weekend bags at public courses. In that market, the lasting edge is not the hardware itself—it is the dataset the hardware generates over time. A decade of shot-level data across 36,000+ mapped courses is not something a new entrant can replicate quickly. That archive is the backbone of the AI-driven coaching and recommendation features that keep users locked into the platform. The model mirrors what reshaped connected fitness: hardware gets the device onto the bag, subscription keeps the relationship alive month after month.

AI-driven sports platforms have been drawing attention from larger consumer technology players precisely because recurring subscription economics compound in ways that one-time hardware sales do not. GYGY is a company running that same model in a sport with one of the most loyal customer bases in all of consumer recreation—execution is what the commercial launch will prove. What’s New At Game Your Game, Inc. (Nasdaq: GYGY) GYGY Completes Its Nasdaq Direct Listing On July 30, 2026, GYGY announced its shares would begin their first session on the Nasdaq Capital Market. CEO Soumya Das called the listing a defining milestone and said the company is focused on completing its commercial launch, scaling its subscriber base, and building on the GameGolf AI platform. GYGY Strengthens Its Board Leadership

In a July 30, 2026 filing, GYGY announced two key board appointments. Soumya Das became chairperson of the board, while Adam Benson joined as an independent director and will serve as the audit committee’s financial expert. Up To $40M In Potential Capital Support

GYGY also put a sizable capital arrangement in place ahead of its commercial expansion. According to the company’s filing, GYGY entered into a Securities Purchase Agreement with Streeterville Capital, LLC on June 30, 2026, providing for potential purchases of up to $40M in Series A preferred shares over time.Streeterville’s relationship with GYGY began even earlier. According to Renaissance Capital, the firm provided financing to the company in March 2026 with an implied common equity reference price of $8 per share.For a company moving from beta testing toward a broader commercial launch, the agreement gives GYGY another potential source of capital as it works to expand the GameGolf KZN AI platform and grow its subscriber base.

7 Reasons Why GYGY Is Topping Our Watchlist This Morning —Tuesday, August 11, 2026… 1. Small Float: With less than 500K shares listed as available to the public, GYGY’s small float could witness the potential for big swings if demand begins to shift. 2. Newly Listed On The Nasdaq: Having completed its Nasdaq direct listing on July 30, 2026, GYGY is one of the newest names on the exchange. 3. Rapid Revenue Growth: with trailing twelve-month revenue up approximately 293% year over year during its beta-testing phase, GYGY is entering full commercial launch from a growing early-stage base. 4. Massive Data Library: backed by an estimated 300M+ recorded shots, more than 3M rounds, and 36,000+ mapped courses, GYGY has accumulated more than a decade of golf-performance data. 5. AI Golf Platform: through GameGolf KZN AI™, Smart Caddie, neural-network sensors, GPS tracking, and personalized recommendations, GYGY combines artificial intelligence with real-world golf performance data. 6. Global Golf Reach: with its technology already used across more than 140 countries and a worldwide golf audience estimated above 108M players, GYGY is addressing a large international market. 7. Capital Support: through an agreement providing for potential purchases of up to $40M in Series A preferred shares, GYGY has established an additional source of funding as it works to expand its platform and subscriber base.

Take A Look At GYGY While It’s Still Early…

When you put all seven pieces together, GYGY becomes a name worth taking a look at before Tuesday morning. The company is newly listed on Nasdaq, has less than 500K shares listed as available to the public, and is entering full commercial launch after posting approximately 293% year-over-year revenue growth during its beta-testing phase. Behind that sits more than a decade of golf-performance data, including an estimated 300M+ recorded shots, more than 3M rounds, and 36,000+ mapped courses. Through GameGolf KZN AI™, Smart Caddie, neural-network sensors, and GPS technology, GYGY is using that data to build an AI-powered platform for golfers around the world. Its technology has already reached users in more than 140 countries, the worldwide golf audience is estimated above 108M players, and the company has an agreement in place providing for potential purchases of up to $40M in Series A preferred shares as it works to expand its platform and subscriber base. That is a combination of a small float, a fresh Nasdaq listing, rapid early-stage revenue growth, a large proprietary data library, AI technology, global reach, and potential capital support—all coming together as the company moves into its commercial launch. We have all eyes on GYGY this morning. Take a look at GYGY while it’s still early—under 90 minutes to go. Sincerely, Alex Ramsay

Co-Founder / Managing Editor

Krypton Street Newsletter |