Any content you receive is for information purposes only. Always conduct your own research.

*Sponsored

Paul Prescott Puts (Nasdaq: SAFX) On The Watchlist This Morning — Monday, August 10, 2026

Don’t Miss Our Next Update—Get Real-Time Alerts Sent Directly To Your Phone. Up To 10X Faster Than Email. Put SAFX On Your Screen While It’s Still Early…

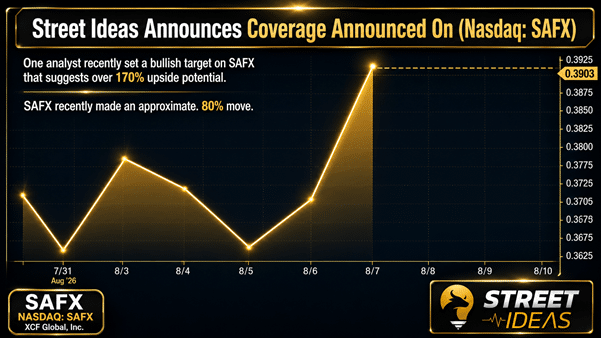

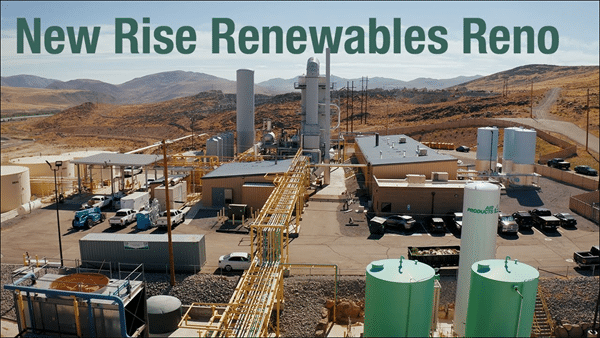

August 10, 2026 Dear Reader, The story Street Ideas brought to readers last night has not slowed down — and the bell is about 90 minutes away. On Friday, August 7, 2026, XCF Global, Inc. (Nasdaq: SAFX) confirmed in an operational update that New Rise Renewables Reno had produced renewable diesel and completed initial fuel sales following its planned upgrade program. CEO Chris Cooper described the next phase: "Restarting a renewable fuels facility is only the beginning. Our focus now is operating safely, improving reliability and executing with discipline as production and commercial activity advance." Initial sales are moving forward under the July 7, 2026 definitive agreements with BGN INT US LLC — and that framework is working. According to Benzinga, Amit Dayal at H.C. Wainwright set a $1 Bullish target on SAFX suggesting over 170% upside potential from Friday's $0.37 range — before initial fuel sales were confirmed. Catching this for the first time this morning? Here is the one thing worth knowing before the open: earlier this summer, SAFX made an approximate 80% move in under a month per Barchart — and every milestone that followed came after that move.

The August 7 operational update is the headline — but the SAFX story stretches well beyond Reno. On April 13, 2026, XCF signed a definitive Business Combination Agreement with Southern Energy Renewables and a Nasdaq-listed carbon management company. Southern Energy brings a planned 28M-gallon-per-year eSAF project in Louisiana, while the carbon management partner adds an environmental asset platform tied to low-carbon fuel activity. A preliminary proxy was filed July 27, 2026, with July 29 as the shareholder record date. XCF has outlined 2027 targets of $775M–$825M in gross product sales, $110M–$120M in net revenue, and $65M–$70M in EBITDA — all set before initial fuel sales at Reno were confirmed. On the policy side, the 45Z Clean Fuel Production Credit runs through December 31, 2029, while D4 RINs under the Renewable Fuel Standard and California's LCFS can add further value depending on fuel pathway, carbon intensity, feedstock eligibility, and other applicable requirements. XCF's Reno facility runs on waste- and residue-based feedstocks including used cooking oil, animal fats, and agricultural co-products. SAFX heads into Monday with several developments moving at once — initial fuel sales confirmed, commercial ramp advancing, three-party combination moving through the shareholder process, and policy credits running through the end of the decade. For Street Ideas, that is more than enough reason to keep SAFX on the radar. The Company Behind SAFX — What Is Operating, What Is Signed, And What Is Still Coming

XCF Global is a Houston, Texas-based producer of renewable diesel and sustainable aviation fuel. Its flagship facility, New Rise Renewables Reno, sits in Nevada with a permitted nameplate capacity of 38 Mln gallons per year. The plant runs on HEFA technology under an Axens license with Alfa Laval pretreatment equipment, converting waste- and residue-based feedstocks — used cooking oil, animal fats, agricultural co-products — into renewable diesel, renewable naphtha, and blended SAF. Here is what makes the current moment worth paying attention to. Following a planned upgrade program, the facility restarted operations, produced renewable diesel, and completed initial fuel sales — with ongoing optimization work designed to support reliability and long-term commercial performance. That sequence matters: upgrade, restart, production, sales. Six months ago this was a development-stage story. Today it is an operating one. XCF came to Nasdaq through a business combination with Focus Impact BH3 Acquisition Company. The commercial backbone of Reno's operations is the BGN INT tolling agreement — six years, covering 100% of feedstock supply and positioning BGN INT as the priority offtake partner for all renewable fuel produced at the facility. That agreement converted a prior binding term sheet into a fully executed commercial framework. The feedstock is sourced. The buyer is contracted. The conversion is happening. That is the operating picture at Reno right now. The platform does not stop there. Beyond Reno, the development pipeline includes New Rise Reno 2, Fort Myers FL, Wilson NC, and a 15-year international licensing agreement with New Rise Australia covering three facilities in Western Australia, South Australia, and Queensland. The pending three-party merger with Southern Energy Renewables and a Nasdaq-listed carbon management company — with a preliminary proxy filed July 27, 2026 and a shareholder record date of July 29 — would expand that platform significantly if closed. What exists today at Reno is the starting point, not the ceiling. Microsoft, Google, Amazon, Nike, FedEx, UPS, and DHL All Want SAF — And There Are Only 40 Facilities Producing It

Microsoft, Google, Amazon, Nike, FedEx, UPS, and DHL have all made formal SAF purchasing commitments as part of Scope 3 emissions strategies. That list is not a group of airlines. It is a cross-section of the global economy — and every one of those companies is looking for fuel that domestic production is not yet built to supply at scale. That is the sector SAFX operates in. And it has a supply problem that is not going away soon. Aviation cannot electrify at commercial scale in the near term. Battery-electric aircraft are not viable at range or payload. Hydrogen-powered flight remains years from deployment. SAF is the only pathway that exists right now — a chemical drop-in for conventional jet fuel that works in existing aircraft and existing infrastructure, reducing lifecycle carbon emissions by up to 80% without a single modification to the planes burning it. The supply gap is severe. Roughly 40 facilities produce SAF globally today. Getting to net-zero aviation by 2050 requires something closer to 7,000. Annual global SAF demand is expected to reach approximately 5.5 Bln gallons by 2030, according to XCF's corporate presentation, against current capacity that covers a fraction of that. The U.S. SAF Grand Challenge targets 3 Bln gallons of domestic annual production by 2030. New Rise Reno is one of only five SAF-capable facilities operating in the United States. XCF is producing. Blending mandates across the EU, UK, China, India, Canada, and Brazil are adding regulatory demand on top of those voluntary corporate commitments — demand that domestic production is not yet positioned to satisfy on either front. U.S. jet fuel prices climbed roughly 70% year-over-year as of mid-2026, driven by disruptions to conventional crude supply routes. Renewable fuel produced from local waste feedstocks carries a cost structure with no exposure to Middle Eastern crude benchmarks. That supply chain independence is what fuel buyers — from airlines to logistics operators to corporate sustainability teams — are actively asking for. XCF is producing that fuel today. The SAFX Story In Six Steps — From Definitive Merger Agreement To Initial Fuel Sales

- XCF confirmed that New Rise Reno had produced renewable diesel and completed initial fuel sales following its planned upgrade program — reported on August 7, 2026.

- XCF filed a preliminary proxy statement tied to its three-party business combination, with July 29, 2026 set as the shareholder record date — filed on July 27, 2026.

- New Rise Renewables Reno began producing renewable diesel, marking the transition from commissioning to expected revenue-generating operations — announced on July 9, 2026.

- XCF executed definitive agreements with BGN INT US LLC, establishing a six-year tolling structure covering 100% of feedstock supply with BGN INT as priority offtake partner — executed on July 7, 2026.

- Amit Dayal at H.C. Wainwright initiated Bullish coverage on SAFX with a $1 target, ahead of the July production start and the subsequent initial fuel sales confirmation — initiated on June 23, 2026.

- XCF signed a definitive Business Combination Agreement with Southern Energy Renewables and a Nasdaq-listed carbon management company, with combined 2027 gross product sales targets of $775M–$825M — signed on April 13, 2026.

7 Reasons We Are Watching SAFX First Thing Monday Morning — August 10, 2026… 1. 170% Upside Potential: Amit Dayal at H.C. Wainwright set a $1 Bullish target on SAFX — suggesting over 170% upside from its recent $0.36 range, according to Benzinga — and that target was set before initial fuel sales were confirmed.

2. Approx. 80% Move First: SAFX made an approximate 80% move in under a month this past summer — from around $0.33 on June 16 to $0.60 on July 10 per Barchart — before the production milestone and before first sales were confirmed.

3. Sales Are In: New Rise Reno completed initial renewable diesel sales per the August 7 operational update — the company has crossed from production into commercial execution and the focus is now on the ramp ahead.

4. Upgrade Behind Them: The planned upgrade program at New Rise Reno is finished — lower-temperature operating parameters and updated process conditions are now in place, and the facility is advancing through its commercial ramp.

5. BGN INT Active: Initial fuel sales are proceeding under the six-year tolling structure with BGN INT — covering 100% of feedstock supply and serving as priority offtake partner for all renewable fuel produced at New Rise Reno.

6. Merger In Process: A definitive business combination with Southern Energy Renewables and a Nasdaq-listed carbon management company is working through the shareholder approval process — with combined 2027 gross product sales targets of $775M–$825M established before initial fuel sales at Reno were confirmed.

7. Credits Through 2029: The 45Z Clean Fuel Production Credit — up to $1.75 per qualifying gallon, extended through December 2029 — stacks with D4 RINs and LCFS credits to build a multi-layer regulatory revenue base around SAFX's fuel production. Put SAFX On Your Screen While It’s Still Early…

SAFX is the name Street Ideas is watching heading into Monday — and the story behind it has not finished moving. New Rise Reno has moved into initial fuel sales, the planned upgrade is complete, and the facility is advancing through its commercial ramp. SAFX has already shown strong recent momentum, including an approximate 80% move from June 16 to July 10, according to Barchart. Amit Dayal at H.C. Wainwright has placed a $1 Bullish target on SAFX, which suggests over 170% upside potential from Friday's $0.37 range, while the BGN INT framework and pending three-party business combination add more developments to watch. At Street Ideas, we put names in front of readers when the developments warrant it — and right now, SAFX warrants it. Our next update could be coming very soon. Keep an eye out for it. Sincerely, Paul Prescott

Co-Founder & Managing Editor

Street Ideas Newsletter |