MSTR vs JPMorgan: Inside the Proxy War for Bitcoin’s FutureWhy Wall Street’s biggest bank and Bitcoin’s largest corporate holder are suddenly on a collision course and how to trade it

For months, something has been brewing beneath the surface of the market. A tension you can feel but can’t quite name. It finally snapped into view on October 10, when MSCI released a quiet consultation paper that landed like a grenade inside the Bitcoin ecosystem. The proposal sounded technical. Companies with more than half their assets in crypto might no longer qualify as ordinary equities. They might be reclassified as digital asset treasuries and removed from core global indices. A single rule change that could force billions of dollars in passive outflows. MicroStrategy, the largest corporate holder of Bitcoin on the planet, was the immediate target. Then JPMorgan stepped in. The bank issued a research note warning that the MSCI treatment could trigger two point eight to eight point eight billion dollars in forced selling. Bitcoin had already fallen from its spring highs. Liquidity was thin. The warning hit the tape like a precision strike. BTC slid toward the mid eighty thousand range. MicroStrategy fell harder. Bitcoin supporters erupted. A boycott of JPMorgan trended on X within hours. Accusations of coordinated pressure, short selling, and a new version of Operation Chokepoint flew across feeds. That single moment exposed a much bigger conflict. This is not a normal market rotation. It is not simply a debate about index rules. It is a proxy war over the future of corporate Bitcoin and the role of banks in a world where money can move without them. The evidence points to two competing theories. Both are deeply informed by public filings, price action, and institutional behavior. Both explain part of the story. And both reflect a simple truth. Bitcoin is no longer a curiosity in the financial system. It is a structural threat. And MicroStrategy is the first company to challenge the banks on their own playing field.

In this article I am going to lay out both theories clearly, with sourced evidence and no speculation. Then we will step back and look at the bigger question that actually matters. How do you position yourself so that you can potentially profit no matter which side turns out to be right? By the time you finish reading, you will understand the battle lines. You will understand why this conflict matters. And you will have a practical strategy designed for exactly this kind of moment. Let’s break down what is actually happening. The Rise of the Corporate Bitcoin StandardYou cannot understand this conflict without understanding what MicroStrategy has become. It is no longer a business intelligence company in any practical sense. It is a Bitcoin operating company that used traditional capital markets to accumulate more than six hundred forty nine thousand BTC. Roughly three percent of the entire global supply. More than many countries. Seventy plus percent of its balance sheet is now Bitcoin. It is also leveraged. MicroStrategy issued convertible debt, preferred stock, and equity to build this position. When Bitcoin goes up, the leverage helps. When Bitcoin goes down, the stock shows brutal volatility. Over the past year, MicroStrategy has underperformed Bitcoin by a wide margin even though the correlation sits near zero point ninety four.

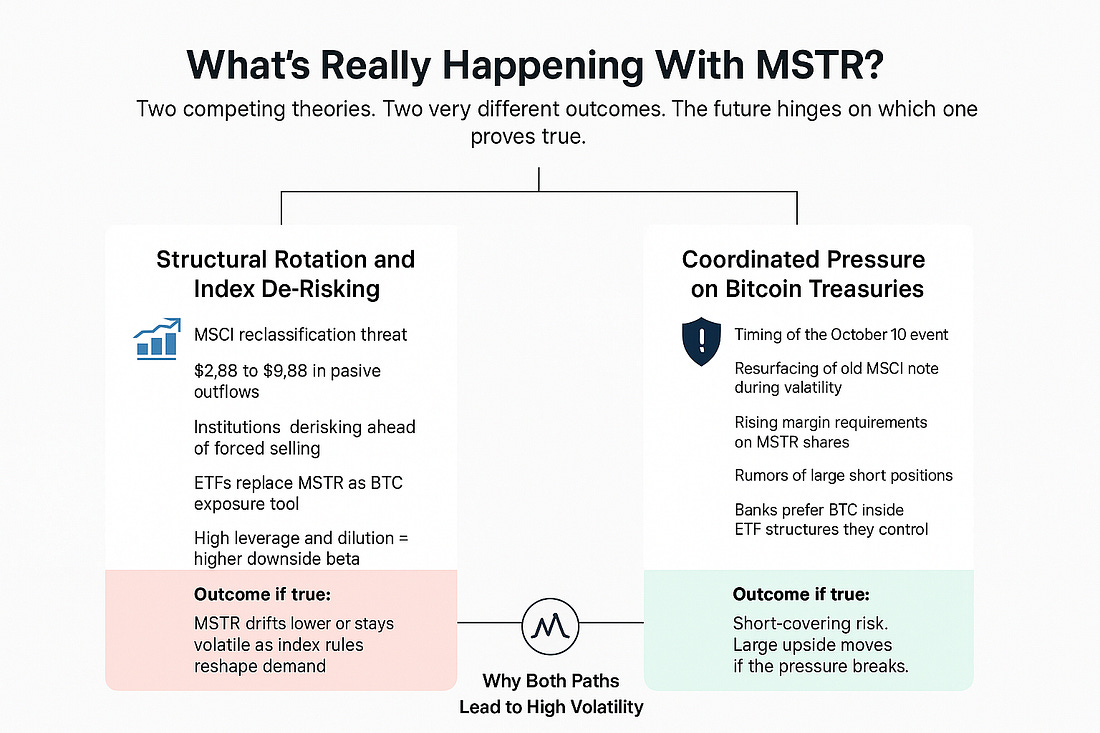

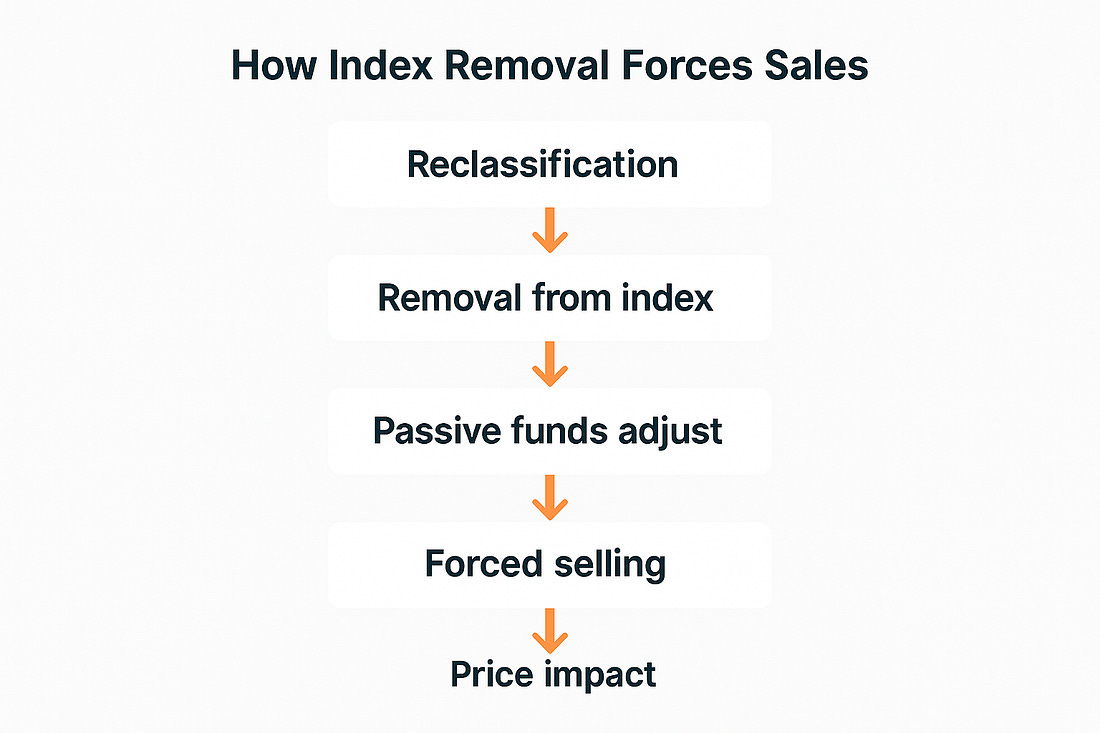

Before the ETF era, institutions used MicroStrategy as a Bitcoin proxy. Post ETF, they do not need it anymore. Now, they can buy the asset directly with daily liquidity and institutional custody risk controls. This shift is important. It is one of the reasons the stock has diverged from Bitcoin’s direction. It sets the stage for the first theory. Theory One: The Structural Rotation and Index De-RiskingThis is the most conservative explanation and the one supported by explicit filings and institutional behavior. It goes like this. MSCI’s consultation would treat companies like MicroStrategy as if they are funds rather than operating businesses. If that happens, passive index funds would be forced to sell. JPMorgan estimates that this could trigger two point eight billion dollars in mechanical selling if MSCI alone moves forward. If S&P and Russell follow, the number could climb toward nine billion dollars.

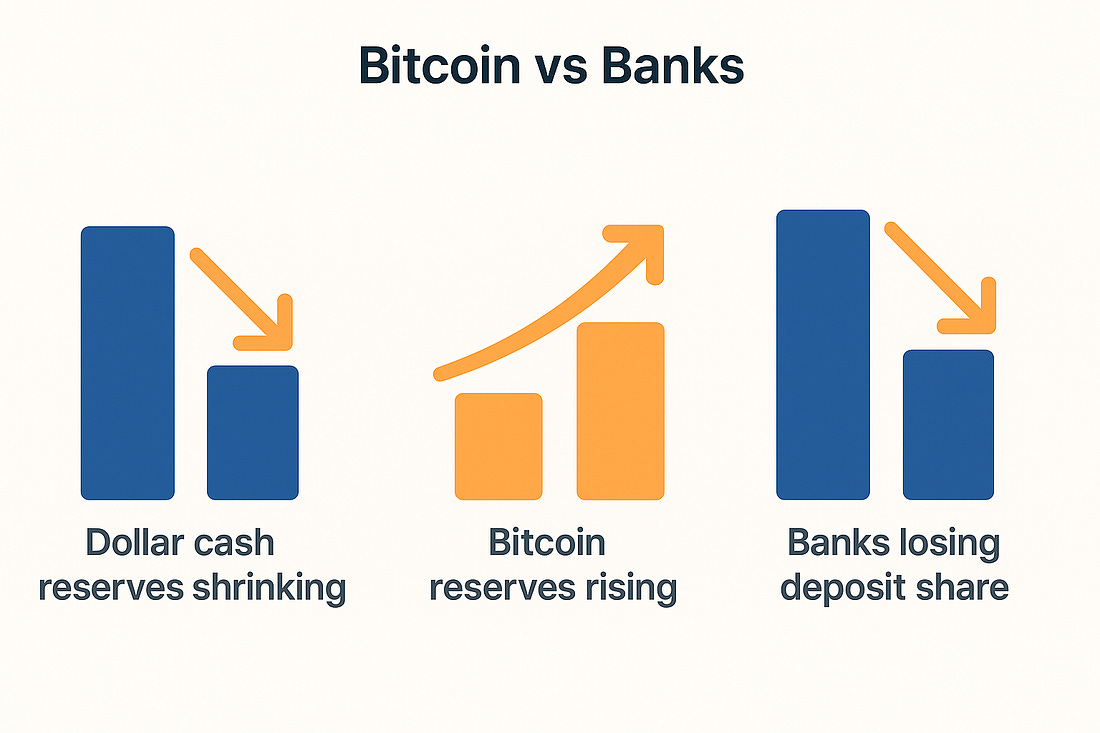

Large institutions do not wait for forced selling. They reduce exposure ahead of time. That is exactly what happened. In the third quarter of 2025, JPMorgan reduced its MicroStrategy position by roughly twenty four percent, selling more than seven hundred seventy thousand shares. BlackRock and Vanguard also trimmed positions. This was not quiet retail trading. These were calculated moves by firms managing trillions. From their perspective, MicroStrategy is a leveraged Bitcoin vehicle with dilution risk, debt risk, and index removal risk. Now that spot Bitcoin ETFs exist, they have no structural need to hold the stock. Under this theory, JPMorgan’s report was not an attack. It was risk modeling in plain sight. A sober assessment of what index rules mean for a highly volatile asset. This explanation fits the data. It requires no conspiracy. It requires no coordination. It explains the timing of institutional sales and the divergence between Bitcoin and MicroStrategy’s stock. But it does not explain the intensity of community backlash. It does not explain the patterns that Bitcoin analysts point to. And it does not address the core truth at the center of this story. Bitcoin threatens the banking system. Which brings us to the second theory. Theory Two: Coordinated Pressure to Contain Corporate BitcoinThis theory is far more controversial. It does not rely on hidden documents. It relies on observable patterns and incentives. The argument goes like this. MicroStrategy is the first major corporation to adopt Bitcoin as a primary treasury asset. It is the proof of concept that a publicly traded company can escape the gravity well of the dollar and build a capital structure tied to Bitcoin instead of bank credit. If MicroStrategy succeeds and other firms imitate it, banks lose one of their core levers of power. Deposits shrink. Lending pipelines weaken. High margin services erode. Settlement flows bypass the interbank system. In that world, JPMorgan needs Bitcoin exposure, but only inside structures the bank controls. ETFs. Structured notes. Custodial products. Not sovereign corporate treasuries holding the asset directly. So when MicroStrategy grows too large and begins to behave like a parallel banking entity, the pressure begins. The October ten event is the flashpoint here. Critics allege that JPMorgan resurfaced a weeks old MSCI note during a period of high volatility, coinciding with tariff announcements and thin liquidity. The result was a nineteen billion dollar liquidation cascade across Bitcoin markets. This remains an allegation, not a proven fact. But the timing ignited the idea that JPMorgan was more than an observer. On top of this, Bitcoin community analysts cite evidence of rising margin requirements, rumors of large short positions, synchronized institutional selling, and the abrupt shift in index classification narratives. MicroStrategy’s removal from S&P five hundred consideration in September also fits this worldview. Not as an isolated decision, but as part of a broader resistance to corporate Bitcoin adoption. The theory does not claim JPMorgan wants Bitcoin to die. Far from it. The bank is already launching Bitcoin linked products and participating in ETF liquidity. The claim is that JPMorgan wants Bitcoin contained inside walls it controls. And MicroStrategy is outside those walls. Why Bitcoin Is a Real Risk to JPMorganBoth theories share a common root. Bitcoin is not a speculative token anymore. It is a competing monetary system that threatens the foundations of modern banking. Here is why. Bitcoin transactions do not require settlement intermediaries. That means no fee extraction. No float. No opaqueness in credit exposure. Bitcoin does not rely on deposits. That means banks lose funding base power.

Bitcoin works twenty four seven, cross border, and without counterparty risk. That undermines the very product line banks sell when they create, move, and price credit. MicroStrategy takes this even further. By issuing debt to buy Bitcoin, the company is creating a Bitcoin denominated capital structure. Something that looks like the early stages of a Bitcoin yield curve. A world where money markets build on Bitcoin instead of bank liabilities. If this model spreads through corporate America, JPMorgan faces an existential problem. The financial plumbing it built for a century becomes optional. That is the core truth under everything happening right now. Where the Evidence LeadsThe structural rotation theory is well supported. JPMorgan’s modeling is public. Institutional sales are documented. Index rules are real. The coordinated pressure theory has no smoking gun but carries significant circumstantial weight. Timing. Incentives. Market behavior. Narrative control. The sharp contrast between JPMorgan’s public skepticism of Bitcoin and its private appetite for Bitcoin linked instruments. Both theories can be true at the same time. A structural rotation can happen while an incumbent financial power quietly applies pressure to contain a threat. This is why MicroStrategy has become the battleground. It sits at the intersection of both systems. The banking system built on credit and the emerging system built on Bitcoin. And that friction is not slowing down. It is accelerating. The First Corporate Bitcoin War Has StartedThis is bigger than a stock. Bigger than an index rule. Bigger than a research report. This is the first direct collision between a corporation operating on the Bitcoin Standard and a global bank built on the dollar standard. MicroStrategy represents the idea that corporations can hold their own monetary energy. JPMorgan represents the world where banks hold it for them. What happens next will shape the future of corporate treasuries, capital markets, and long term monetary power. The next phase begins when MSCI finalizes its decision. And the market reaction to that decision will tell you which side is gaining ground. A Strategy That Profits Whether JPMorgan Is Right… Or the Bitcoin Maxis Are RightThere is a very clean way to play this situation. It works whether this turns into a structural derisking event that hammers the Bitcoin corporate proxy… or whether MicroStrategy rips higher in a face-melting short squeeze. The key is to stop thinking like a stock picker and start thinking like a volatility trader. Right now you have:

When the market misprices both tails, the highest expectancy trade isn’t directional. It’s long convexity. Below are three versions of the same idea. You can pick whichever matches your risk appetite... Continue reading this post for free in the Substack app

|

MSTR vs JPMorgan: Inside the Proxy War for Bitcoin’s Future

الاشتراك في:

تعليقات الرسالة (Atom)

0 التعليقات:

إرسال تعليق