| | | Would a $1 Trillion OpenAI IPO Make Any Sense? | | | |

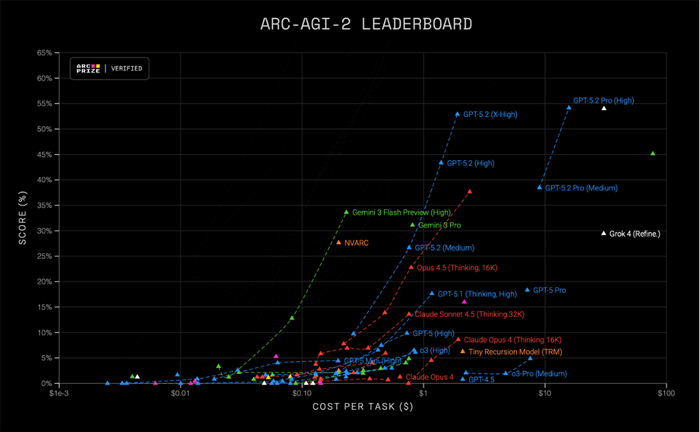

Well, we've just about made it. What an absolutely crazy year this has been. | | I'm going to have a bit of a different publishing schedule for the next two weeks. My team has worked really hard this year, and I'm giving them a break to enjoy the holidays for the next couple of weeks. We'll still be publishing daily, though. | | We've lined up some of our favorite Bleeding Edge issues from 2025 for you, discussing everything from the oncoming age of space exploration to how AGI is going to permanently change the landscape of labor – and the opportunity therein. | We'll also have our usual AMA issue on both Fridays and are taking questions for those, as always. If you'd like, please write us here. | | On the 31st, I'll publish my year in review, and then on New Year's Day, you can look forward to your first issue of 2026, where I'll publish my predictions for the year. | | The editorial team even had a little holiday fun with the issues leading up to Christmas Day, so be sure to check those out. It should be some great holiday reading. | | I hope that everyone has a wonderful week next week with family and friends. | | Happy Holidays, | | Jeff | | Can OpenAI Regain Ground? | | | Hello Jeff and the whole team, | | | | You raised two crucial points regarding OpenAI's valuation: | | My question concerns the long-term investment opportunity for individual investors. | | Despite these warning signs — lagging behind key competitors and historically high initial valuation — do you consider OpenAI could still represent a "smart investment" over the long term, say 5 to 10 years? | | In your view, what arguments could justify this valuation and potentially turn the company into a sustainable stock market success, even if it is not the first to achieve AGI? | | Thank you in advance for your valuable perspective on what will likely be one of the most debated IPOs in history. | | Have a great day. | | – Cherif K. | | | | Hello Cherif, | | Your question is useful as it is a good example that is applicable to companies experiencing a high level of hype and have incredible growth potential. | | The real question is whether OpenAI can not only grow into its current valuation (i.e., through EBITDA and free cash flow) and grow well beyond that, giving late-stage investors a chance at some kind of return. | | Before we get to that, just last week OpenAI announced, out of its normal product release sequence, its latest version of its frontier AI model – GPT 5.2. | | This was clearly intended to quell the concerns of those investors who were worried that OpenAI was falling behind Google's Gemini 3 Pro and xAI's Grok 4. | | The release of GPT-5 was such a flop. I'm sure the pressure was on to get the model back on track and closer to best in class, at least on some metrics. | | To be fair, GPT-5.2 did deliver top results in a few categories. One that I wrote about in yesterday's Bleeding Edge was the ARC-AGI-2 benchmark… GPT-5.2 is the first to score above 50%. | | | | Source: ARC Prize | | But on most common benchmarks, Gemini 3 Pro or Grok 4 comes out on top right now. Google's latest release of Gemini is really impressive, and xAI is holding back its next release of Grok until the end of December or early January. And Grok 5 is expected in the March/April timeframe. | | OpenAI is by no means out of the race. It is just behind. | | As for what arguments could be made to justify its current valuation… | - We would have to believe that OpenAI is going to grow revenues to at least $50 billion by 2027 to justify its current $500 billion valuation.

- We would have to believe that OpenAI is going to reach its forecasted revenue of $100 billion by 2028 to justify a $1 trillion valuation at IPO.

- We would have to believe that OpenAI can maintain and monetize roughly 70% of its global market share for generative AI.

- We would also have to believe that OpenAI can grow its market share in its enterprise-related business.

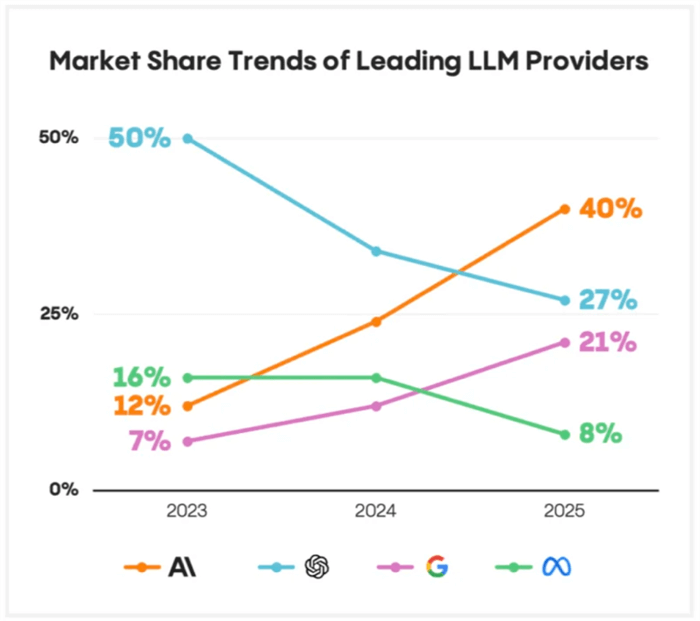

| | The risks are fairly obvious right now. OpenAI's market share for generative AI has actually been shrinking. At the moment, Google is OpenAI's largest threat because Google already has the largest distribution channel to end users on the internet through its search engine market share. | | And this year, OpenAI lost the top spot for enterprise generative AI API-related business by a wide margin to Anthropic. | | | | Source: Menlo Ventures | | With all this said, the winner hasn't been named yet. It is still a frenetic race. I believe that the leaders will be redefined in a matter of months once the first company launches a powerful personalized agentic AI that has integrated with payment systems. The adoption rates will be like nothing we've ever seen before. | | The other catalyst will be whoever gets to AGI first, and how long the gap will be between the first to AGI and the second or third. That's why time is so important, and there is so much investment happening right now to build out AI factories. First to market provides an extraordinary competitive advantage. | | Ironically, xAI carries the lowest valuation of the big three at $230 billion, versus Anthropic's most recent valuation at $350 billion and OpenAI's $500 billion. | | From my perspective, xAI has the largest potential gain given its technology and latest valuation, and OpenAI carries the most risk… which is ironic, considering it was "first to market" in the sense that it was OpenAI's release of ChatGPT in November 2022 that catalyzed the AI fervor of the past few years. | | I've argued that the timing of these discussions by OpenAI to go public next year is suspicious. While exciting, it is early for a company still burning so much cash and early on in its mission. | | As an analyst, I have to objectively consider what the OpenAI board must be thinking. One argument for going public early is that they, as insiders, understand the true state of OpenAI's technology and the competitive risks. | | If they know that OpenAI is unlikely to achieve a breakthrough and would be significantly overvalued at a $1 trillion IPO, then they would likely take the company public, provide liquidity to all prior investors, executives, and employees… because they very well know that the valuation will decline. | | Sadly, companies do this all the time and essentially take advantage of those who don't understand valuations. This is my concern about OpenAI and the current discussions surrounding a $1trillion valuation IPO. | | Obviously, as we get closer to the event, I'll certainly provide my thoughts as more details emerge. | | For the moment, we are dealing with imperfect information and have to make our own assumptions and predictions about future business outcomes and technological advancements… which is a whole lot of fun. | | | | Intel's Purpose in AI? | | | What are Intel's plans to make itself relevant once more? What is the U.S. government gaining from its 10% investment in Intel? How does Intel fit into the administration's America First agenda? | | In April, you noted the new CEO and said, "Intel's product roadmap is now the most aggressive I've seen in years." Could you expand on and update your understanding of their roadmap? How does Intel plan to compete and coexist with companies like Taiwan Semiconductor, Nvidia, Broadcom, and Micron, and participate in the AI data center buildout like those other companies? What will be Intel's purpose in this AI ecosystem? | | How do the semiconductor manufacturing equipment companies Applied Materials, ASML, KLA, Tokyo Electron, Lam Research, and Teradyne compare and compete? Foundry companies like Taiwan Semiconductor, Samsung, and Intel appear to need equipment from many or all of these companies to fabricate semiconductors. Does their equipment compete, is it complementary, or are different companies' equipment components that require one another? | | How does electronic design automation software from Cadence Design Systems, Synopsys, and Siemens (Mentor Graphics) compare and contrast? How does design software fit with the semiconductor manufacturing equipment? How do semiconductor design companies like Nvidia and Broadcom design their chips and deliver their designs to the foundries so they can fabricate the chips? | | Does design software run in part on GPUs? If so, how does it leverage AI capabilities? How is the software used to design semiconductors also used to design other complex systems? | | Thanks. | | – Bobby W. | | | | Hi Bobby, | | That's certainly a lot, I think you have more than 20 questions there. I'm afraid I'm not going to be able to answer everything to the level of detail that you might like, as it would probably take about 100 pages to do that properly. But I will try to provide you with useful information at a high level to address your interests. | | Let's tackle Intel first. The latest CEO, Lip Bu Tan, has taken steps this year to refocus the company and refine its product development, as well as get its foundry business back on track. In April, I was happy to see him sell the majority interest in its FPGA division, which was the Altera division. I had been arguing to do that for years. | | Tan also decided not to try and compete directly with NVIDIA – and AMD for that matter – on GPUs. Intel missed that opportunity, and there is no way they would be able to catch up. | This was the impetus for NVIDIA's $5 billion investment into Intel, which is focused on integrating NVIDIA's GPU technology with Intel's CPU technology. NVIDIA was willing to make this investment in an effort to put its largest competitor – AMD – at a disadvantage. | | TSMC is both a competitor and a partner for Intel. Most people don't know that Intel pays TSMC to manufacture its highest-end CPUs. It's embarrassing for Intel, but it is true. Intel competes with TSMC in its foundry business, which is Intel's contract manufacturing business. | | In truth, Intel isn't really a competitor because Intel's foundry business is primarily used for manufacturing its own semiconductors, and its process technology is so far behind TSMC, it can't compete. | | This is one of the areas where Tan is trying to get Intel back on track. It is also the reason for the U.S. investment in Intel. Intel is the only U.S. company that has a shot at being a counterbalance to Taiwan's TSMC, and TSMC always comes with the risk of a China takeover of Taiwan. | | So the idea is to have secure supply chains and at least one U.S.-based company capable of manufacturing leading-edge semiconductors. | | Intel will likely lean into its 14A manufacturing process, which has not been commercialized yet but would put Intel roughly on par with what TSMC is doing. Intel still has to prove it. | | On the product side, Intel will continue to lean into its x86 architecture CPUs, and also its AI accelerators for inference. It competes with AMD on the CPUs (AMD has the highest performance products) and a large number of smaller semiconductor companies on the accelerator side of the business. | | As for the companies that you asked about, generally: | - AMSL – photolithography machines, the most advanced of which are EUV

- Applied Materials – semiconductor manufacturing equipment, also LCD panel manufacturing equipment

- Teradyne – test equipment for semiconductors, also a large industrial robotics division

- KLA – semiconductor manufacturing equipment, famous for metrology and inspection tools

- Tokyo Electron – semiconductor manufacturing equipment

- Lam Research – semiconductor manufacturing equipment, well known for its deposition and etching tools

| | ASML is in a category of its own. When it comes to the most advanced semiconductor manufacturing processes, it is without competition. If Intel is successful with its 14A process, then it might compete with ASML's EUV process. But that's a big "if." | | Intel, Samsung Electronics, and Global Foundries (GFS) all compete with TSMC as contract manufacturing businesses, but none of them can compete against ASML at the most advanced processes. | | And yes, all four of the foundries mentioned above use ASML machines, as well as the others listed above. Applied Materials, KLA, Tokyo Electron, and Lam Research are all in the same bucket and compete with one another. Any company that manufactures its own semiconductor uses a mix of these companies' manufacturing equipment. Teradyne is in a different class, as it is most well-known for test equipment for the semiconductor industry. | | It is worth noting that not every chip needs to be an advanced semiconductor, which is to say not every chip needs to be manufactured using an ASML machine. Chips for the automotive industry, or the consumer electronics industry, or household electronics often use semiconductors manufactured with technology that might be 10 years old. | | ASML's and Teradyne's technology is largely complementary to the other four semiconductor manufacturing equipment names mentioned. | | The two heavyweights in the electronic design automation are Cadence Design Systems (CDNS) and Synopsys (SNPS), which compete directly with each other. Every semiconductor company in the world uses one or both of their software platforms for designing semiconductors. | | Once a semiconductor has been designed, here's what happens: | - The design is first tested and verified to be ready for manufacturing

- The design file is used to create a photomask

- The photomask is used in a lithography machine to project the design patterns onto the silicon wafers

- The circuits are etched onto the silicon wafer, and metal is deposited onto the wafer (deposition)

- The finished wafer is then tested for functionality, for yield, and to identify and mark any defects

- The wafer is then cut up into individual semiconductors – we refer to this as the "dies"

- Then the dies are packaged, which means they are attached to hardware that has external pins so that the finished product can be assembled onto a circuit board of some kind

| | And yes, the EDA software does leverage both CPUs and GPUs to run. They didn't use to many years ago. But today, Synopsys and CDS leverage GPUs for parallel processing for computationally intensive tasks like simulation. | That's a lot to digest. I hope that it is helpful. If you'd like to dig deeper on any of these topics, just let us know. | | Nostradamus Brown | | | Hi Jeff, | | I think you should change your name to Nostradamus Brown since you have an uncanny, almost prescient ability to see the future, and, more importantly, pick the select few winners from a broad field of contenders destined to achieve phenomenal success as we approach the future. | | Your calls [over at Exponential Tech Investor] are producing fantastic high-double and, in some cases, even triple-digit gains in my portfolio. | | It's a real pleasure to work with you and your team, and I'm even more proud to be a new Founder Member! Cheers, and please keep up the good work. | | – Gary D. | | | | Hey Gary, | | I now have you to thank for certain members of my team now calling me Nostradamus. Jeff is definitely my preference, though. | | It's great to have you on board, and I'm glad you're enjoying my research. | | I wish there were an easy button, but the truth is that my team and I go to extensive lengths to research and analyze all the industries that we cover. And anywhere there is a growth market, you can bet that we're all over it. | | Having spent decades working in the field around the world in high-tech gave me both an incredible network and an understanding of how companies/governments analyze, select, and deploy technology. | | Working in several prominent technology sectors also gave me the hands-on experience of how technologies fit together. And as an angel investor for the last 20-plus years, I see every crazy idea that you can think of before almost anyone has heard about it. | | And I spend nearly every waking hour researching, traveling, conducting boots on the ground research, on the phone with my network, exploring anything and everything that might be interesting to my subscribers, and potentially a great investment opportunity. | | I won't be right 100% of the time, but my goal is to be as close to that as I possibly can. In this world, when things are changing as fast as they are, I have to be obsessively in tune with the latest developments so that I can connect the dots, put the pieces together, deduce the implications, and accurately predict the future. | | I have to wonder if the following quote will be proven true: | | | Mankind will discover objects in space sent to us by the watchers. | | – Nostradamus | | | | And fortunately, Nostradamus didn't get them all right: | | | The year 1999, seventh month, from the sky will come a great King of Terror: to bring back to life the great King of the Mongols, before and after Mars to reign by good luck. | | – Nostradamus | | | | Hopefully, when all is said and done, I'll have a much longer string of accurate predictions that will run circles around Nostradamus. I'm still young, plenty of time left. And more excited about the future than ever before. | | Jeff (Nostradamus) Brown | | | | | | | Dec 18, 2025 • 5 min read | | | | | | Dec 17, 2025 • 7 min read | | | | | | Dec 16, 2025 • 5 min read | | | | | | | | | | | To ensure our emails continue reaching your inbox, please add our email address to your address book. This editorial email containing advertisements was sent to ahmedwithnour@gmail.com because you subscribed to this service. To stop receiving these emails, click here. Brownstone Research welcomes your feedback and questions. But please note: The law prohibits us from giving personalized advice. To contact Customer Service, call toll free Domestic/International: 1-888-512-0726, Mon-Fri, 9am-7pm ET, or email us here. © 2025 Brownstone Research. All rights reserved. Any reproduction, copying, or redistribution of our content, in whole or in part, is prohibited without written permission from Brownstone Research. | | | | |

0 التعليقات:

إرسال تعليق