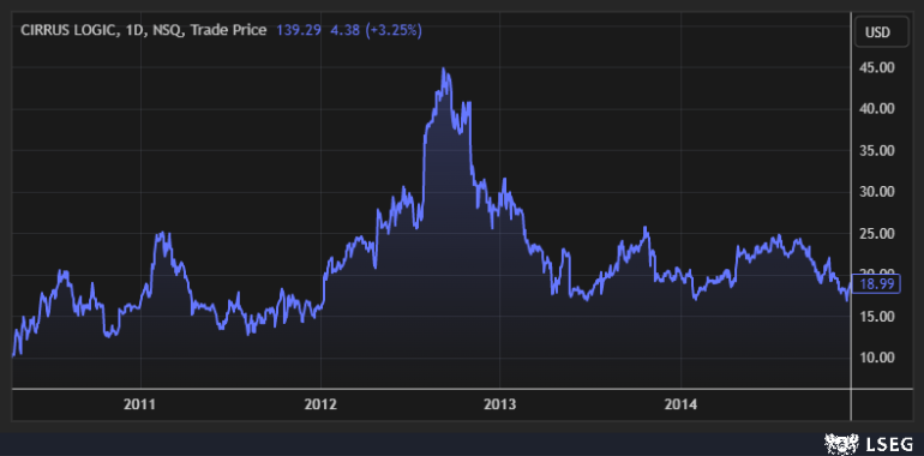

2 Stocks to Buy for AI’s Next Stage VIEW IN BROWSER Tom Yeung here with your Sunday Digest. In the mid-2010s, Wall Street became smitten with finding the next iPhone supplier. Skyworks Solutions Inc. (SWKS)… Cirrus Logic Inc. (CRUS)… Universal Display Corp. (OLED)… These companies often saw their shares jump double-digits when a tech blog or analyst note reported that Apple Inc. (AAPL) had picked them as a supplier. Yet, Apple was often a terrible customer. The smartphone maker famously demanded low prices and high quality, making it almost impossible for physical hardware makers to turn a profit. The charts of many iPhone supplier stocks ended up looking like Mount Everest. Here’s an early-2010s one from semiconductor supplier Cirrus Logic…

Instead, the big winners of the iPhone revolution turned out to be those providing experiences on top of these smartphone systems. Ride-hailing firm Uber Technologies Inc. (UBER), former TikTok owner ByteDance, and mobile advertising company AppLovin Corp. (APP) are now worth more than even the largest iPhone suppliers. A similar scenario is now playing out in artificial intelligence. Last week, we saw a massive selloff in AI’s “infrastructure” companies. Chipmakers… data center developers… power utilities… These suppliers to OpenAI dropped double digits on fears about how much money they were sinking into a profitless industry. InvestorPlace Senior Analyst Louis Navellier believes this is only a warning sign. In a new presentation, he warns that February 25 could be the date when the market faces a sharp AI Dislocation. Expectations are simply too sky-high among these “Stage 1” companies building out the physical side of artificial intelligence. Most investors will either panic-sell or buy the dip in precisely the wrong names… just as they did with iPhone suppliers in years before. Fortunately, Louis believes that a small group of companies still offers ~500% upside thanks to being on the “Stage 2” end of the AI Revolution. You can sign up for the presentation here. In the meantime, I’d like to take two top stocks and illustrate why experience-focused AI companies will become critical, and why now is a great time for long-term investors to start buying the dip in some of these select names. Let’s jump in… | Recommended Link | | | | There is no AI future without nuclear energy, and Luke Lango believes the U.S. Government is preparing to make its own massive move in this sector. You see, one of the companies involved in this nuclear renaissance solves a critical problem the White House is desperate to fix: National security. Luke believes this specific company is next in line for a direct government equity stake. He identified the pattern months ago and tracked the political connections… and now the window to get in before the government announcement is closing fast. Click here to get the details before it’s too late. |  | | The AI Legal Expert In 2009, Google added legal document search to its Google Scholar search engine. Many feared it would replace LexisNexis and Westlaw – the two dominant legal research platforms of the day. Google monopolized other search fields. Why not law as well? But that never happened. You see, legal research doesn’t just require speed. It also needs evaluations, notes, secondary analysis, and other information that doesn’t show up in court briefs and rulings. Law firms additionally require airtight accuracy – something that no large language model (LLM) can guarantee. That’s why Thomson Reuters Corp. (TRI) should eventually dig out of the 60% selloff that began in the middle of last year. The Westlaw owner has spent the past several decades creating the best-in-class legal research portal, and virtually every important court ruling (especially from appellate courts) is collected, researched, and vetted for significance. Much of the legwork is now done by AI, of course, but humans still check the final product. In addition, Thomson Reuters has meticulously curated its other brands. The company sold its position in the London Stock Exchange in 2024 and used the cash to buy AI-focused acquisitions, including Additive (AI-powered tax document processing) and SafeSend (“last mile” automation of tax returns). The company also acquired Casetext in 2023, an early adopter of AI-powered legal research (now called CoCounsel). Growth is therefore expected to remain in the upper single digits, while net profits should rise twice as quickly. Now, it’s certainly possible for AI companies to muscle in on Thomson Reuters’ businesses. After all, Alphabet Inc. (GOOG) is 100 times larger and could still crush the smaller firm by outspending it. But doing so would mean hiring an entire team of salespeople, legal experts, and customer service agents to sell a Westlaw competitor… not to mention the work of annotating briefings, taking customer phone calls, and making database changes when errors are discovered. That would quickly become an enormous distraction for any tech firm. Outfits like OpenAI and Anthropic are even less likely to compete with Thomson Reuters. These AI startups are racing to build the next generation of LLMs… and getting bogged down with creating a Westlaw competitor is a surefire way to fall behind. Instead, these LLM firms are more likely to sell their AI product to Thomson Reuters and let the legacy firm handle the experience of using AI for legal research. So, even though it might take a while for sentiment to improve, shares of TRI should eventually recover. According to my models, it has a 105% upside from here – an excellent investment for any long-term buyer. The AI Provider to the Fortune 500 ServiceNow Inc. (NOW) has spent the past two decades building out a platform that reduces complexity in IT and business processes. The company was an early adopter of AI technologies and quickly expanded from its core IT service management (ITSM) business into customer service, talent development, sourcing, order management, and more. Today, ServiceNow’s platform is used by more than 85% of Fortune 500 companies, and the company boasts a sky-high 98% customer retention rate. The software firm is also growing like wildfire. Revenue rose 21% in 2025, and analysts expect another 20% growth this year. Earnings per share are on track to surge 49%. There are two keys to ServiceNow’s success. - Modular System. ServiceNow's platform makes it easy to cross-sell additional services. If an existing customer wants to add a human resources management system, it's a phone call away. Furthermore, each additional product a customer uses increases the amount of data ServiceNow has about the company, making the system even more powerful. Roughly 75% of customers use multiple ServiceNow products.

- Artificial Intelligence. The second “secret sauce” of ServiceNow is the high quality of its AI systems. The company’s data analytics product is reportedly even better than those offered by AI darling Palantir Technologies Inc. (PLTR), and its development team has worked quickly to make dedicated AI agents for specific tasks, such as customer service and IT.

The plain fact is that ServiceNow should continue to grow because future AI projects will need structure. No matter how advanced OpenAI’s and Anthropic’s systems become, these chatbots need a platform to ingest data, come to conclusions, and do so in a repeatable way. In other words, ServiceNow controls the experience that companies have in working with large language models. The company is also valued at a tiny fraction of high-flying rival Palantir. In fact, ServiceNow could triple its share price and still be cheaper on virtually every valuation metric. And so, I see the recent selloff as an opportunity to buy ServiceNow. Investors might be panicking about some software stocks for the right reasons… but concerns about ServiceNow are clearly overblown. What GPT-5 and 5G Have in Common 5G technologies were an incredible leap forward when they were launched in 2019. The mobile data network used high frequencies, multiple bandwidths, and a more efficient network core that regularly transferred 500 megabits per second of data – more than enough to watch a high-definition movie on smartphones. If 4G was a two-lane road of data, then 5G is a 12-lane interstate on a quiet weekend. Interestingly, the biggest 5G winners were not the infrastructure companies that allowed 5G technologies to exist. Shares of AT&T Inc. (T) and Verizon Communications Inc. (VZ) have fallen since 2019. Instead, the greatest success stories were firms like Netflix Inc. (NFLX), TikTok, and Apple – the companies that stream videos and provid the smartphones that display this entertainment. Every $10,000 invested in Netflix in 2019 was worth $35,000 by 2025. Similarly, OpenAI’s GPT-5 represents a generational leap ahead in AI technologies. GPT-5 and its close rivals are now good enough to perform research… write code… and look a little like the 5G leap forward. And much like 5G, the winners are increasingly looking like the “Stage 2” companies that come after the infrastructure gets built. That’s why last week’s selloff of all AI-related companies was totally unwarranted. Many of these are “Stage 2” specialists that use AI themselves to provide a better product. And crucially, these companies provide the human-AI hybrid that guarantees accuracy in the way that pure AI models cannot. That’s why my colleague Louis Navellier just released his brand-new AI Dislocation broadcast. In this free presentation, Louis explains why a whole new cohort of AI stocks could succeed current “Stage 1” winners. It's a group of firms that will dominate in a world where AI experience matters more than raw computing power. To learn more about these under-the-radar “Stage 2” AI stocks, click here. Until next week, Thomas Yeung, CFA

Market Analyst, InvestorPlace |

0 التعليقات:

إرسال تعليق