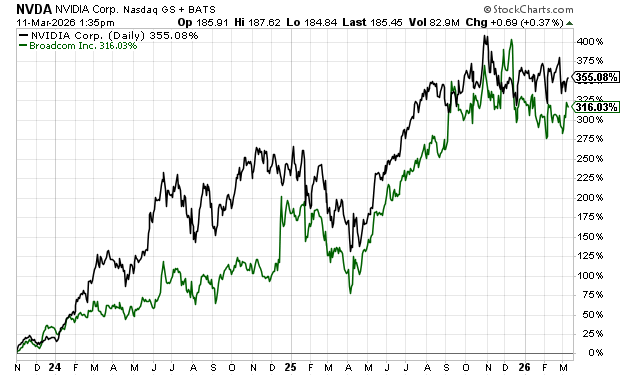

JPMorgan writes down software loans… the risk of private lending and AI… what to make of Oracle’s rally yesterday… why caution is the right response… Eric Fry says this is where the next AI boom will take place VIEW IN BROWSER Yesterday, JPMorgan Chase did something subtle – but it’s the kind of move that should make investors sit up a little straighter. The nation’s largest bank quietly began marking down the value of certain loans tied to private-credit portfolios, many of them loans to software companies. It didn’t receive much attention, overshadowed by the Iran war and oil prices – but when a financial giant like JPMorgan starts adjusting the value of collateral behind a booming lending market, it’s worth asking why. Here’s CNBC with more details: The bank is potentially among the first major lenders to pull in leverage to the private credit industry, in a move that mirrors steps taken during Covid, said a person with knowledge of the matter… The bank’s giant Wall Street trading division has reduced the value of loans — most of which were made to software firms. Now, on its own, this adjustment might not seem like a major event. But it comes at a moment when one of the fastest-growing areas of global finance – private credit – is becoming increasingly intertwined with another of the market’s most explosive trends… AI. Investors need to trade carefully… You see, a growing share of that private credit is now funding companies racing to build AI data centers and cloud infrastructure – a capital-intensive business where profits are far less certain than the demand for the raw materials powering it. And this disconnect between spending and profits is where risks – and opportunities – are beginning to emerge. To unpack this, let’s start with the debt piece… Private credit has ballooned into a multi-trillion-dollar industry over the past decade As regulators tightened bank lending after the 2008 financial crisis, private lenders stepped in to fill the gap, offering loans to companies that traditional banks might hesitate to finance. For borrowers, the appeal is flexibility. For lenders, the appeal is yield. But the entire system rests on a simple assumption: borrowers will continue generating enough cash flow to service their debt. Many of those borrowers operate in technology and software – industries that are currently pouring enormous sums of money into AI infrastructure. The bet is that those enormous sums of money will eventually produce massive new revenue streams. But that’s far from certain. Which brings us to another headline from yesterday involving one of the companies right at the center of the AI boom… Oracle’s surge – and the gamble beneath it Yesterday, Oracle shares jumped as much as 14% after the company reported strong quarterly results and reassured investors about its ability to finance its aggressive expansion of AI infrastructure. During the company’s earnings call, Oracle executives emphasized that the firm does not plan to raise additional debt in 2026 beyond what it has already announced, and that the overall economics of its buildout still works. Here’s Oracle CEO Clayton Magouyrk: We continue to get better and better at running these data centers, delivering them more cheaply, optimizing the amount of cost for networking and hardware spend, as well as power. This message was clearly designed to calm investors’ nerves about Oracle’s massive spending on AI data centers – and it worked. Wall Street interpreted Oracle’s earnings results and the comments about funding data centers as a bullish sign – “demand is strong and the spending race is still manageable!” But still, investors piling into yesterday’s ORCL rally are making a huge gamble – one that our macro expert Eric Fry decided wasn’t worth it when he exited Oracle last fall, even after leading his Investment Report subscribers to a 27% gain. To be fair, Oracle isn’t the only company making this risk bet. Here’s Eric explaining this broader gamble behind the AI boom: Everyone seems to believe that AI is a miracle, but no one seems to know what this miracle means. All that we know for certain is that AI isn’t free. The price tag for the technologies and infrastructure that enable AI will run into the trillions of dollars, but the payoff for this investment remains as inscrutable as a Delphic oracle… Imagine going into a grocery store where no item showed a price tag, and you didn’t discover the total cost until you passed through the checkout line. AI is that grocery store. | Recommended Link | | | | The U.S. government just started building a vast critical mineral stockpile. It’s known as Project Vault – and the White House has already pledged $10 billion to fund it. And it could send these five stocks soaring. |  | | This uncertainty isn’t just theoretical When you start digging into the economics behind the AI infrastructure boom, the numbers can get uncomfortable very quickly. Eric’s lead analyst in Fry’s Investment Report, Tom Yeung, recently walked through an illustration using Oracle, which was part of the reason why Eric sold. Last September, Oracle signed a massive agreement to provide cloud computing capacity to OpenAI. Here’s Tom breaking down the numbers: Oracle signed a $300 billion cloud deal to provide 4.5 gigawatts of cloud computing power to OpenAI between 2027 and 2032. We know that each data center gigawatt costs roughly $50 billion to build – $35 billion for Nvidia chips, and another $15 billion for everything else… That means Oracle will spend around $225 billion through 2027 ($50 billion × 4.5) to build these data centers to make $300 billion in revenue. Now, if everything goes perfectly, the project could generate enormous profits. But the margin for error is thin. If a major customer delays spending… if pricing pressure emerges… or if AI demand doesn’t materialize as expected, those economics could change very quickly. And remember, Oracle doesn’t have some massive technological edge in its AI, which puts even more weight on the economics of these deals. Back to Tom: At its core, AI computing is a service that’s mostly indistinguishable between providers. They all use the same Nvidia Corp. (NVDA) chips running on the same platform. So, choosing between providers usually comes down to price. That’s not an ideal setup for companies spending hundreds of billions of dollars to build AI infrastructure while betting on future revenue to justify the investment. Circling back to private lending, we’re already seeing hints of stress in the financing ecosystem supporting this buildout. For example, private credit giant Blue Owl Capital – a major lender to technology and software companies – recently faced a surge in redemption requests from investors in one of its funds, forcing the firm to restrict withdrawals and sell roughly $1.4 billion in loans to raise liquidity. Bad AI loans were not the cause specifically. But it highlights something important: a huge share of private-credit lending today is tied to software companies whose business models may themselves be disrupted by AI. And that’s exactly the kind of scenario JPMorgan’s quiet loan markdown may be hinting at. So, where should investors look instead? Where Eric sees the smarter opportunity Eric believes the smarter move is to focus on the parts of the economy that will benefit from AI’s expansion, regardless of which software companies ultimately win. Increasingly, those parts are the industry’s bottlenecks – the critical inputs the entire system depends on. We’ve already seen how powerful those opportunities can be. After all, when an industry hits a bottleneck, the companies that solve it often capture enormous gains. To illustrate, let’s begin with Eric describing one of the earliest bottlenecks of the AI era: In November 2023 – just a year after ChatGPT’s debut – OpenAI CEO Sam Altman made a surprising decision. He suspended signups for ChatGPT’s paid subscriptions, cutting off new users from OpenAI's advanced models. Demand for ChatGPT had exceeded the company’s GPU capacity. One of the most advanced AI companies in the world had run out of ‘compute.’ There weren’t enough chips, networking components, or infrastructure to power the AI explosion. In effect, the entire industry hit a wall. That compute bottleneck turned out to be incredibly lucrative for the companies positioned to solve it. Nvidia (NVDA) and Broadcom (AVGO) – two firms sitting directly in the path of that infrastructure shortage – delivered enormous gains for early investors as the AI boom accelerated. Below, you can see AVGO and NVDA soaring 316% and 355% respectively since November 2023:

But as Eric explains, the compute bottleneck that fueled those early gains is now beginning to ease…which means the next phase of the AI boom will likely revolve around entirely new constraints. Where the next bottlenecks – and opportunities – are forming According to Eric, the next wave of AI opportunities is coming from the industries that supply the physical inputs the AI economy depends on. Take copper, for example. Every data center, circuit board, transformer, cable, and chip requires it. And the scale of future demand is staggering. As Eric notes: To maintain current growth rates, we would have to mine the same amount of copper in the next 18 years as humanity mined during the previous 10,000 years combined. That’s the kind of physical constraint that can reshape entire industries. But copper is only the beginning… AI data centers require enormous amounts of electricity to operate. They depend on specialized memory chips to run AI models. And they rely on complex supply chains of metals, cooling systems, networking equipment, and power infrastructure. In other words, while software may capture the headlines, the real-world infrastructure behind AI may ultimately determine how fast – and how profitably – the entire industry grows. That’s why Eric is urging investors to shift their attention – and their investment dollars – toward the companies solving these physical bottlenecks. He’ll be explaining exactly where those opportunities are during a special event called FutureProof 2026 next Wednesday, March 18 at 1 p.m. ET. Here’s Eric: During this free broadcast, I’ll explain why shortages in metals, electricity, and memory are becoming the next major bottlenecks in the AI boom – and why investors who identify these constraints early could position themselves for the next wave of gains. I’ll bring you more details in the coming days, but you can reserve your spot for Eric’s FutureProof 2026 broadcast right here. Wrapping up… JPMorgan’s headline yesterday is a reminder that parts of today’s financial system may be taking on more risk than investors realize – especially as trillions of dollars flow into AI infrastructure. Oracle’s rally shows the excitement is still alive. But as Eric and Tom point out, the real question isn’t whether AI will change the world – but whether every company spending billions will earn an attractive return. So, is there a better bet? If history is any guide, yes – own the companies supplying the tools, materials, and infrastructure that the entire system depends on. More on how Eric is doing this over the next few days… Have a good evening, Jeff Remsburg |

0 التعليقات:

إرسال تعليق