Dear Reader, Dr. Mark Skousen here. I've worked for the CIA. I've personally met four US presidents. I've spent 45 years studying the markets — calling Black Monday six weeks before it happened... predicting the fall of the Berlin Wall... pinpointing the exact bottom in 2009. But what I'm about to share with you is the boldest prediction of my career. After meeting Elon Musk face-to-face at a private gathering of Wall Street elites, I'm now staking my reputation on one date. March 26, 2026. Mark it on your calendar right now! That's when I believe Elon will announce the SpaceX IPO — what Bloomberg is calling "the biggest listing of ALL TIME." I have an "access code" that lets you grab a pre-IPO stake before it happens. But I'm only willing to share it with 500 people today. After that, you my never get the chance again. Click here to see how to claim your “SpaceX access code”. Yours for peace, prosperity, and liberty, AEIOU, Dr. Mark Skousen

Macroeconomic Strategist, The Oxford Club P.S. I don't make predictions lightly. When I put my name on something, I mean it. Click here before the 500 spots are gone.

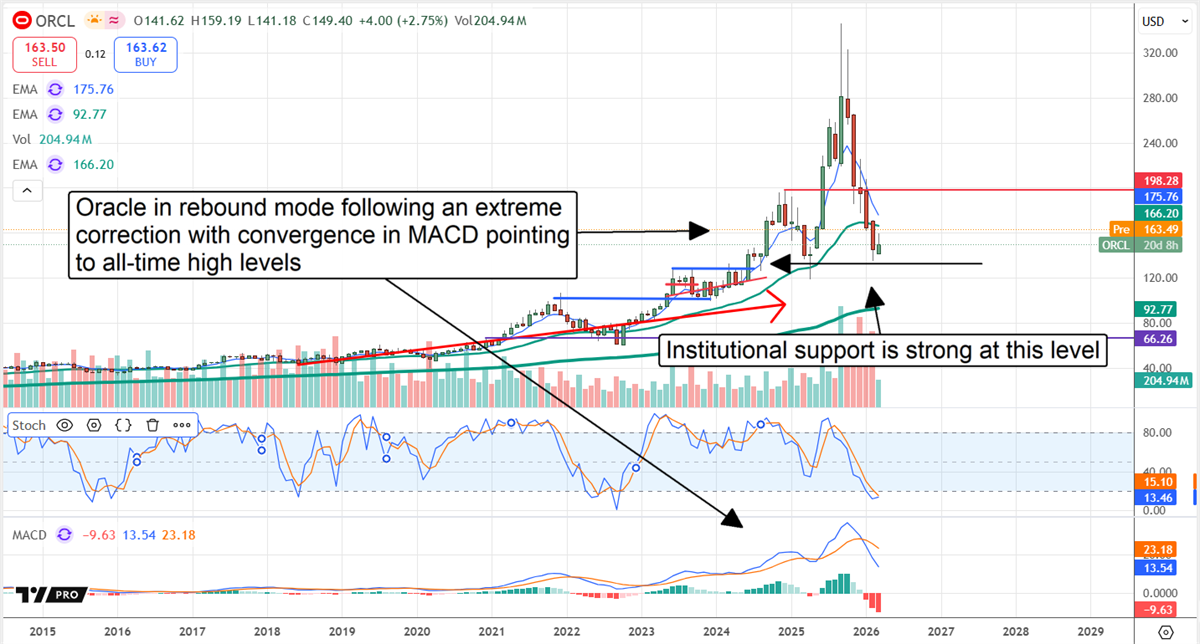

Today's Bonus Content Oracle Speaks! The Message: AI Demand Outpaces CapacityAuthored by Thomas Hughes. Publication Date: 3/11/2026.

Key Points- Oracle's Q3 release affirms its robust outlook and upped the ante with improved long-term guidance, and the analysts liked it.

- Price target increases and upgrades point to rising share prices and the potential for a robust rebound and fresh all-time highs.

- Institutions accumulated in Q1 when prices were low, providing a support base and limiting risk in 2026.

- Special Report: Nvidia CEO Issues Bold Tesla Call (From Brownstone Research)

Oracle’s (NYSE: ORCL) stock could be poised for the hottest upswing in modern tech history. The company’s fiscal Q3 2026 report not only affirmed a robust outlook and eased debt-related fears, it also raised forward guidance. The takeaway for investors is succinct: in the words of JPMorgan (NYSE: JPM) analysts (who upgraded the stock), the results provide some of the clearest proof yet that Oracle’s AI strategy is working. Oracle is emerging as a powerhouse of AI innovation, offering infrastructure, development tools, and AI-driven applications while improving services for both legacy and new clients. Analysts, Institutional Buying, and Price Action Align: Robust Rebound BrewingA major force in the crypto world is quietly becoming one of gold's most aggressive buyers — and most investors have no idea it's happening.

A longtime gold analyst says profits from a leading stablecoin operation are being funneled into physical gold at a scale that could materially impact supply and demand. After a recent meeting with insiders, he began outlining what this trend could mean for gold prices and a small group of companies positioned to benefit. Read the full gold briefing here Analysts are responding as expected—reaffirming bullish outlooks, issuing upgrades, or raising price targets. Sentiment has swung back to an aggressively bullish posture, reversing earlier price-target cuts, strengthening the Strong Buy consensus, and improving the rebound outlook. Right now the bias is firmly bullish: 75% of ratings are Buy or better, the lone Sell rating is over a year old, and the consensus price target implies roughly an 80% upside from the pre-release close, with momentum pointing toward the high end of the range. The high end is pegged at $400—more than 165% upside—and could be reached well before year-end. Institutional trends also support a price-bottom thesis and an outlook for sustained upward momentum. Although institutions sold on balance in Q4 2025, that bearish behavior ended with the new year as they switched back to accumulation. Early Q1 activity shows more than $1.50 bought for every $1 sold, creating a net tailwind that is likely to strengthen as the year progresses. The charts reinforce the narrative: daily, weekly, and monthly indicators suggest the stock was significantly oversold and is set up for a bullish momentum swing. The most likely near-term outcome is a retest of the all-time high, with potential to exceed it either by a base-case $140 in dollar terms or by as much as a 100% percentage gain. A break to new highs would signal trend continuation and open the path to those upside scenarios.

Oracle Rebounds on Outperformance and Acceleration Oracle delivered its strongest quarter in more than 15 years in Q3. Revenue rose over 21% to $17.19 billion, accelerating both sequentially and year-over-year (YOY), and outpaced consensus by 165 basis points. The strength was broad-based, led by a 44% increase in total cloud revenue. Total cloud grew 44% to nearly $9 billion, representing roughly 52% of revenue. Cloud infrastructure surged 84%, driven by a 531% increase in Multi-Cloud Database and a 243% gain in AI infrastructure. SaaS revenue grew 13%, with Fusion and NetSuite contributing meaningfully. Margins and earnings were also strong. Oracle leveraged revenue growth to beat consensus adjusted earnings estimates across the board despite higher spending and increased debt. Adjusted EPS of $1.70 exceeded consensus by a substantial margin (590 basis points), generating healthy cash flow and positioning the company for continued strength. Guidance should further lift the stock now that the rebound is underway. Oracle issued hot guidance for Q4, implying better-than-forecast full-year results and raising its outlook for the following year. The company now expects revenue growth to accelerate to over 31% annually, outpacing estimates for both revenue and earnings. A major driver will be rapid expansion of cloud and AI capacity, with at least another 14 hyperscaler instances (roughly a 25% increase) expected to come online in the near term. Oracle’s Debt: Not So Much a Concern as a NeedOracle’s debt and share count have increased to fund its expanding AI network. While debt concerns are understandable, they reflect necessary financing to capture a fast-growing opportunity. Q3 results and a swelling backlog—now about $553 million, up 325% YOY—indicate rapid expansion is required, or a competitor will fill the demand instead. Importantly, the backlog remains more than 4.4 times the debt, roughly equivalent to eight years of business at the Q3 pace, and much of that backlog should be recognized sooner. That dynamic should enable rapid debt reduction and meaningfully increase shareholder equity over the coming years. Risks remain—additional capital may be needed—but they will be mitigated if backlog growth continues as forecast.

This ad is sent on behalf of The Oxford Club. 105 W Monument St, Baltimore, Maryland 21201. If you would like to optout from receiving offers from The Oxford Club please click here |

0 التعليقات:

إرسال تعليق