| | | This week delivered the sharpest geopolitical reversal we've seen all year. Trump promised an exit on Tuesday and escalation on Wednesday — and markets got caught in the middle. Traditional safe havens are acting like risk assets, energy bottlenecks are tightening, and Friday's jobs data lands on a closed market. |

| | |

| In this issue, we answer: |

| ✭ Why did gold lose $100 in minutes after a 4-day rally? | ✭ What happens to oil supply now that the Hormuz pipeline is empty? | ✭ How should you read Friday's jobs data if markets don't open until Monday? | ✭ Exclusive from American Hartford Gold: Why Central Banks Are Dumping Dollars for Gold |

|

|

|

| | | | Geopolitics Whipsaw Gold and Oil | Let's look at the raw data from this week. On Tuesday, President Trump signaled that U.S. forces could leave Iran within two to three weeks, claiming the nuclear threat was handled. Futures jumped, and oil briefly dipped below $100 a barrel as traders priced in an off-ramp, which you can track via this market breakdown. But by Wednesday night, the narrative completely flipped. In a prime-time address that lasted under 20 minutes, Trump promised to hit Iran "extremely hard" over the next few weeks, talking about sending them back to the Stone Ages.

| The market reaction was immediate and aggressive. Hopes dimmed for a swift end to the conflict, sending oil prices surging back above $105 a barrel. Meanwhile, gold — which had been on a four-day recovery, climbing as high as $4,800 earlier that day — took it on the chin. COMEX gold futures dropped roughly 2.2% to around $4,677 per ounce, and spot gold fell about 2% to $4,664 by early Thursday. The move erased more than $100 intraday, snapping gold's winning streak right after Trump's speech signaled escalation. | Investors are getting whiplash trying to front-run the geopolitical headlines. The fundamental truth here is that rhetoric moves markets in the short term, but actual supply chains and troop movements dictate the long game. We've got a situation where the initial relief rally was a mirage. When the commander-in-chief changes his stance in 24 hours, the smart money stops guessing and starts looking at the hard constraints on the ground. |

| | |

| | | | Donald Trump just did it again. | At a rally, he confirmed his Rebate Stimulus Plan — but it's not just about sending out checks. | Behind closed doors, Trump's team is pushing a strategic wealth‑protection move that could matter far more than a one‑time payment. | Why now?

✅ Skyrocketing inflation

✅ A weakening dollar

✅ Markets spinning out | This isn't just a "bonus" — it's a chance to shield your savings from what's coming. | |

| |

| | |

| | | Hormuz Keeps Oil Risk Premium High | The real bottleneck isn't the daily political theater — it's the Strait of Hormuz. After 33 days of conflict, the U.S. hasn't secured control over Iran's oil reserves or that vital waterway. About a fifth of the world's oil flows right through there. Even if the U.S. were to pull out completely without a formal ceasefire, that doesn't magically reopen the maritime routes. The risk premium on oil isn't going anywhere. | Just this Wednesday, a QatarEnergy-leased tanker was hit by an Iranian cruise missile in Qatari waters. That's a hard, physical constraint on global energy supply. The IEA's executive director warned this week that April will be significantly worse than March — the cargo ships that were already in transit when the war began have now been delivered, meaning the pipeline is empty. We're looking at Brent crude hovering around $100–$105 a barrel after previously spiking above $119. Energy disruptions are already threatening to hit the European economy this month. Oil dictates the baseline cost of everything in the American supply chain, and right now, that baseline is highly exposed to ongoing regional strikes. | |

| | |

| | | Inflation Squeeze and Reserve Sales | When energy costs stay elevated, inflation isn't just a lingering threat — it's an active drain on the system. We saw inflation expectations jump in March, and that's forcing a global reaction. Countries are getting squeezed by higher energy import bills. | Turkey sold and swapped roughly 60 tons of gold — worth over $8 billion — in just two weeks after the war began, the largest weekly drawdown in nearly seven years. The Central Bank of Turkey had been one of the biggest gold buyers for 23 straight months. Now it's tapping those reserves to defend a struggling lira. Several European governments are openly debating how to fund surging defense budgets without destabilizing their currencies. Even Petrodollar states in the Middle East, struggling to export oil through the contested Strait of Hormuz, might find themselves liquidating assets to fund basic food imports. | | The pressure cooker is very real. The narrative is shifting from temporary price bumps to entrenched structural costs. The Federal Reserve is watching this closely, waiting to see exactly how these global supply shocks filter into domestic prices. |

| | |

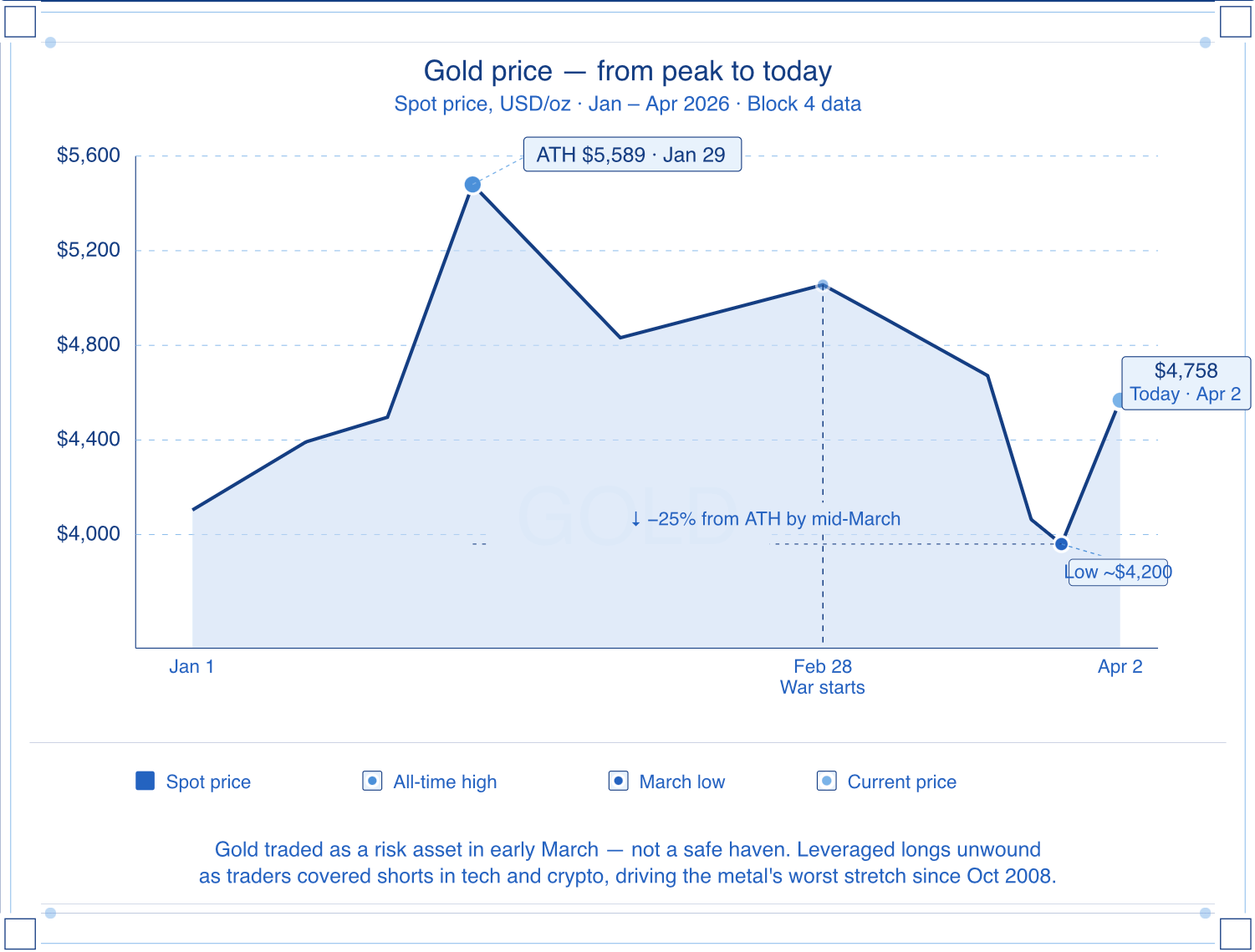

| | | | Gold Acting Like Risk-On, Not Haven | Here's one of the more confusing shifts we've seen since the conflict started: gold has been behaving more like a risk asset than a clean safe haven. Back in January, speculative froth pushed gold to an intraday peak near $5,595 on January 29. | Immense leverage built up. When the war kicked off on February 28, gold did spike initially on safe-haven demand — but that move was short-lived. Traders quickly started liquidating their long gold positions to cover shorts in tech stocks and crypto. | We saw a massive de-grossing of risk, causing gold to plummet roughly 27% from its January peak by mid-March, falling to around $4,090 — its worst stretch in years. At the same time, haven appeal lifted the U.S. dollar, creating a meaningful headwind for gold — a stronger dollar makes the metal more expensive for holders of other currencies. You combine dollar firmness, higher-for-longer interest rate expectations, and a broader liquidity squeeze, and you start to see the hidden risks in traditional wealth preservation models. The old playbook of buying gold the second bombs drop and holding without question is a lot more complicated now. | |

| | |

| | | Jobs Report, Dollar, and the Good Friday Trap | We are heading into a uniquely dangerous data window. The Bureau of Labor Statistics releases the March nonfarm payrolls report this Friday, April 3 — and here's the catch: it lands on Good Friday. Every major U.S. stock exchange will be closed. Bond markets, shut. The data drops at 8:30 AM Eastern into a market that cannot react until Monday morning. | That setup matters. February's print was brutal — the economy shed 92,000 jobs, nearly double what forecasters expected and the worst single-month loss in recent memory. Wall Street consensus for March is a modest bounce to around 57,000 new jobs, partly because the Kaiser Permanente healthcare strike that suppressed February's numbers has since been resolved. But even if that consensus holds, it's still well below the pre-war monthly average. | Here's where it connects to everything above. If the labor market shows resilience while energy-driven inflation stays sticky, the Fed has zero reason to cut rates. Bets on a December rate reduction have already fallen to around 12%, down from roughly 25% before Trump's latest comments. That keeps the dollar firm and puts a hard ceiling on gold and other non-yielding assets. | The broader picture: we're operating in an environment where policy shifts happen overnight, data lands on closed markets, and the next 72 hours will set the tone for April. The smart money isn't trying to guess what Trump says next — it's watching the physical oil flows, tracking central bank liquidity moves, and paying very close attention to how the dollar responds when Monday morning finally arrives. |

| | |

| | | | | - Exclusive Content from American Hartford Gold - |

| | |

|

|

0 التعليقات:

إرسال تعليق